2026 Payroll Changes Every Small Business Owner Needs to Budget For Now

- Suzy Luther

- Feb 20

- 6 min read

If you're running payroll for your small business, the rules just changed: and these aren't minor tweaks. New federal regulations that took effect this year will impact how you report wages, how your employees file their taxes, and how much certain tax credits are worth to your business.

Whether you employ tipped workers, pay overtime regularly, or provide childcare benefits, 2026 brings substantial reporting obligations and new deduction opportunities that require immediate attention. Let's break down exactly what's changing and what you need to do about it.

New Reporting Requirements for Tips and Overtime

The most significant shift involves how you report certain types of compensation on tax forms. Starting with wages paid in 2026, employers must separately report qualified tips and qualified overtime compensation on Forms W-2 or 1099-NEC.

This isn't just a formatting change. You'll also need to include occupation details when reporting tip income: something that wasn't required before. Previously, tips and overtime were typically aggregated with regular wages, but the IRS now wants this information broken out distinctly.

Here's what this means in practice:

If you employ servers, bartenders, or other tipped workers, you'll need to track and report their qualified tips as a separate line item

Overtime compensation must be identified and reported separately from regular wages

You'll need to document the employee's occupation for tip reporting purposes

Your payroll system may require updates to accommodate these new reporting fields

The IRS provided temporary penalty relief for 2025 payments while businesses adjusted their systems, but full compliance is required for all 2026 employee payments. There's no grace period anymore.

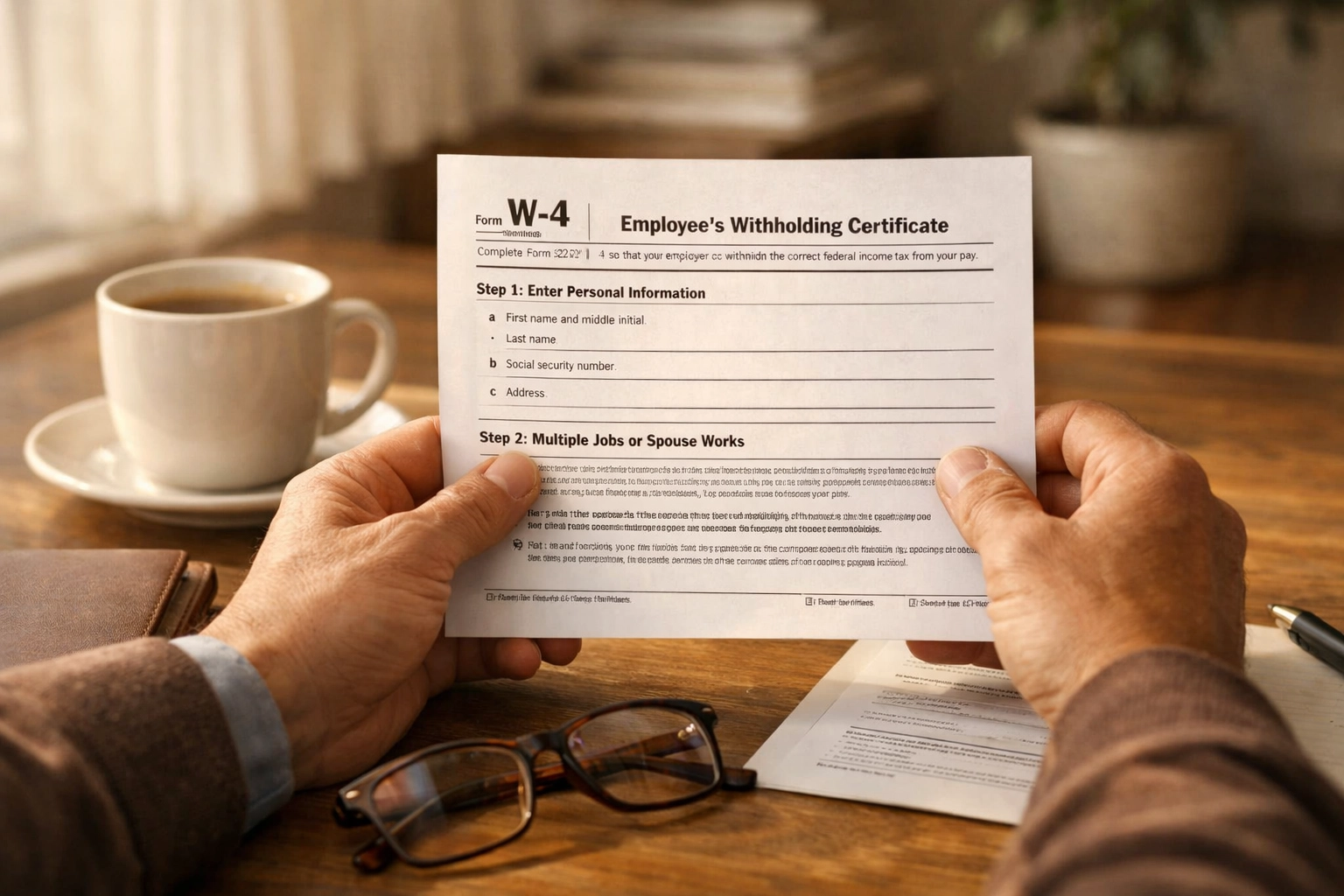

Employee Withholding Adjustments: The New Form W-4

To accommodate these changes, the IRS released updated Form W-4s specifically designed for employees who expect to claim the new tip and overtime deductions. This is an important development because it allows employees to adjust their federal income tax withholding upfront rather than waiting until they file their tax return.

When employees submit these new W-4 forms, they can reduce their withholding to account for deductions they'll claim at year-end. This means more money in each paycheck throughout the year.

As an employer, you should:

Inform employees about the availability of updated W-4 forms

Process new W-4 submissions promptly to adjust withholding calculations

Update your payroll software to properly calculate withholding based on these new deductions

Keep accurate records of which employees have submitted updated forms

This isn't just administrative busywork: it directly impacts your employees' take-home pay and can improve retention and satisfaction when handled correctly.

Employee Deductions That Affect Your Payroll Planning

Two new above-the-line deductions are now available to employees, and understanding them helps you advise your team and anticipate withholding changes.

Qualified Tip Income Deduction

Employees working in IRS-designated tipped occupations can now claim an above-the-line deduction of up to $25,000 annually for qualified tips. This deduction phases out based on modified adjusted gross income (MAGI):

Single filers: Phase-out begins at $150,000 MAGI

Joint filers: Phase-out begins at $300,000 MAGI

For context, if one of your servers earns $40,000 annually with $15,000 coming from tips, they could potentially deduct all $15,000 of that tip income, significantly reducing their taxable income.

Qualified Overtime Compensation Deduction

Employees can now deduct qualified overtime compensation with the following limits:

Single filers: Up to $12,500 annually

Married filing jointly: Up to $25,000 annually

Same MAGI phase-out thresholds as the tip deduction ($150,000/$300,000)

Important clarification: This deduction applies only to the FLSA premium portion of overtime pay: the "half-time" component. For example, if an employee earning $20/hour works overtime at $30/hour, only the $10 premium portion qualifies for the deduction, not the entire $30.

Let's say you have an employee who regularly works 10 hours of overtime per week. At $20/hour regular pay, that's $300/week in overtime ($30/hour × 10 hours), with $100 being the premium portion. Over a year, that's approximately $5,200 in qualified overtime compensation they could potentially deduct: a meaningful tax benefit.

Expanded Employer-Provided Childcare Credit

If you provide childcare benefits or have considered doing so, this change deserves your attention. The employer-provided childcare credit has significantly expanded for 2026.

What Changed

The credit increased substantially:

Standard businesses: From 25% to 40% of eligible childcare costs

Eligible small businesses: Up to 50% of eligible costs

Annual maximum credits: Increased from $150,000 to $500,000 ($600,000 for eligible small businesses)

New Flexibility Options

Small businesses can now pool resources to jointly operate childcare facilities or work through intermediaries and still qualify for the credit. This opens opportunities for businesses that couldn't afford standalone childcare facilities.

Why This Matters for Your Budget

If you're competing for talent in a tight labor market, offering childcare benefits just became significantly more affordable from a tax perspective. A business spending $100,000 annually on qualified childcare expenses could now receive a $40,000-$50,000 credit: double what was available before.

Consider whether adding or expanding childcare benefits might strengthen your employee value proposition while generating substantial tax savings.

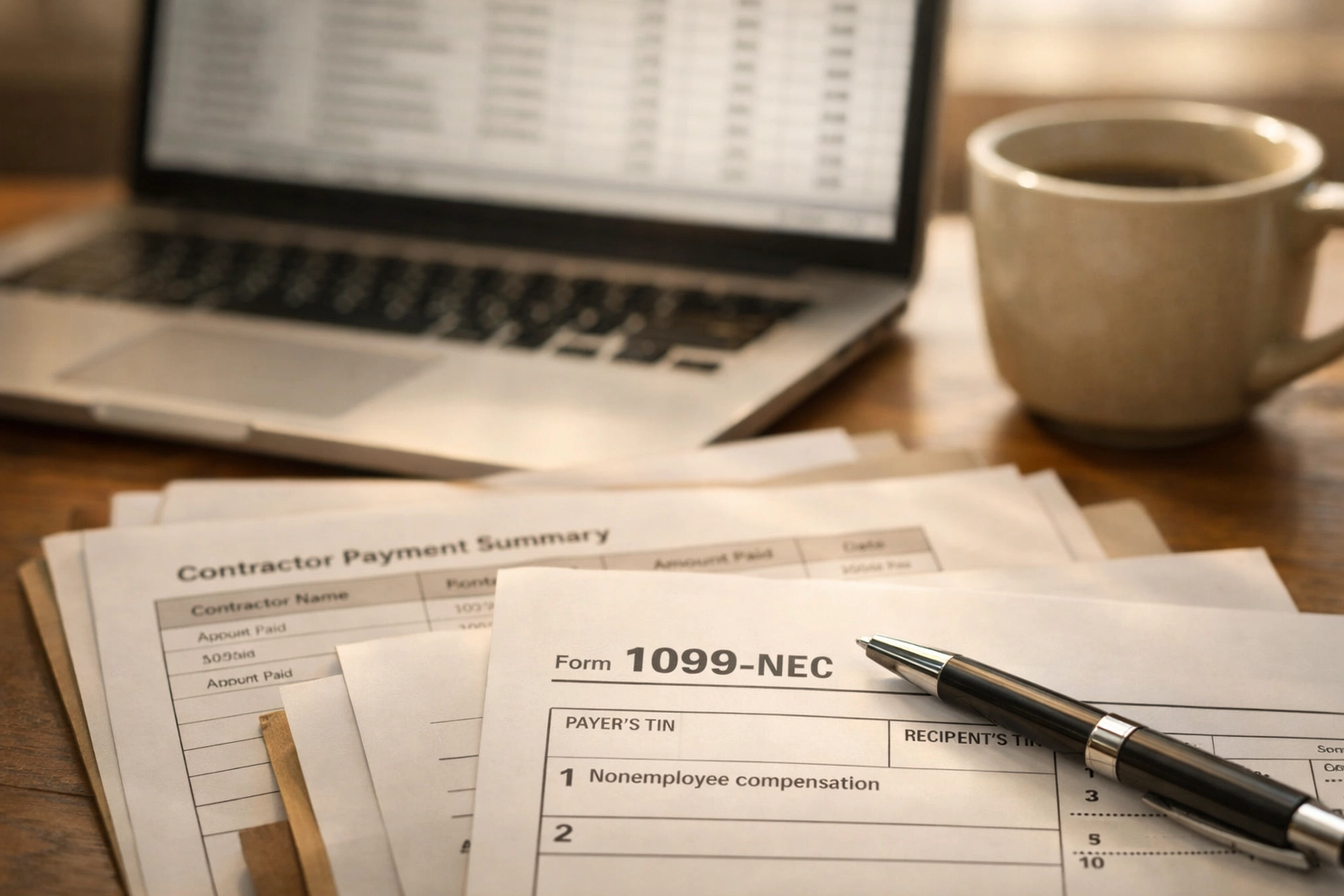

The 1099 Reporting Threshold Increase

There's one change that might actually reduce your administrative burden. The reporting threshold for Forms 1099-NEC and 1099-MISC has increased from $600 to $2,000 for 2026, with future adjustments for inflation.

This means if you paid a contractor $1,500 for services in 2026, you're no longer required to file a 1099 for that payment. However, it's still good practice to track all contractor payments regardless of threshold for your own expense documentation.

Keep in mind:

This applies to payments made in 2026 and reported in early 2027

The threshold applies per payee, not in aggregate

Proper contractor classification remains critical regardless of payment amount

Action Steps: What You Need to Do Now

Don't wait until December to address these changes. Here's your implementation checklist:

Immediate Actions (This Month):

Audit your payroll system: Verify it can separately track and report tips and overtime compensation

Contact your payroll provider: Confirm they've updated their software for 2026 compliance

Review employee classifications: Ensure you know which employees receive tips or regular overtime

Update internal documentation: Modify your payroll procedures to capture occupation information for tipped employees

Within 60 Days:

Communicate with employees: Inform them about new W-4 options and available deductions

Distribute updated W-4 forms: Make them readily accessible to employees who may benefit

Train your payroll team: Ensure everyone processing payroll understands the new reporting requirements

Evaluate childcare benefit opportunities: Run the numbers on whether expanded credits make offering childcare benefits financially viable

Before Year-End:

Test your updated reporting: Process test payroll runs to verify Forms W-2 and 1099 will correctly separate tip and overtime compensation

Document your compliance efforts: Keep records showing when and how you implemented these changes

Review contractor payments: Identify which contractors will or won't receive 1099s under the new $2,000 threshold

Frequently Asked Questions

Do these changes apply to all businesses or just certain industries?

The reporting requirements apply to all employers who pay tips or overtime compensation. The employee deductions apply to workers in designated tipped occupations (for the tip deduction) and any employee receiving FLSA-qualified overtime pay.

What happens if I don't separately report tips and overtime on W-2s?

You could face IRS penalties for incorrect or incomplete information reporting. Since the grace period ended with 2025 payments, non-compliance in 2026 will be subject to standard penalties.

Can employees claim these deductions if I don't change their withholding?

Yes. The deductions are claimed on their tax return regardless of withholding. Updated W-4s simply allow them to benefit throughout the year rather than waiting for their refund.

Should I encourage employees to submit new W-4 forms?

Provide information about the availability and let employees make their own decisions based on their tax situations. You're not required to advise on their personal tax strategy, but making the forms accessible demonstrates you're looking out for their interests.

The Bottom Line

These payroll changes require proactive planning, not reactive scrambling in December. The reporting requirements are mandatory, the deduction opportunities are valuable for employees, and the expanded childcare credit could significantly impact your benefits strategy.

Start by auditing your current payroll processes and systems. Identify gaps between your current capabilities and the new requirements. Then create a timeline to close those gaps before they become compliance problems.

If your payroll feels increasingly complex or you're uncertain about proper implementation, this might be the right time to consider working with a professional. The cost of expert guidance is typically far less than the penalties for non-compliance or the opportunity cost of missing valuable tax benefits.

Need help implementing these changes or reviewing your payroll processes? Contact SociaTax to discuss how we can help ensure your payroll is compliant and optimized for the new regulations.

Comments